2021 FMI Construction Outlook

Years from now, with the benefit of hindsight, we may look back at 2020 as the year when the unprecedented became commonplace. So much of this year has been characterized by unique challenges, persistent uncertainty and lack of clarity about the future. The unpredictability instigated by the pandemic has cut across almost all industries and sections of the economy.

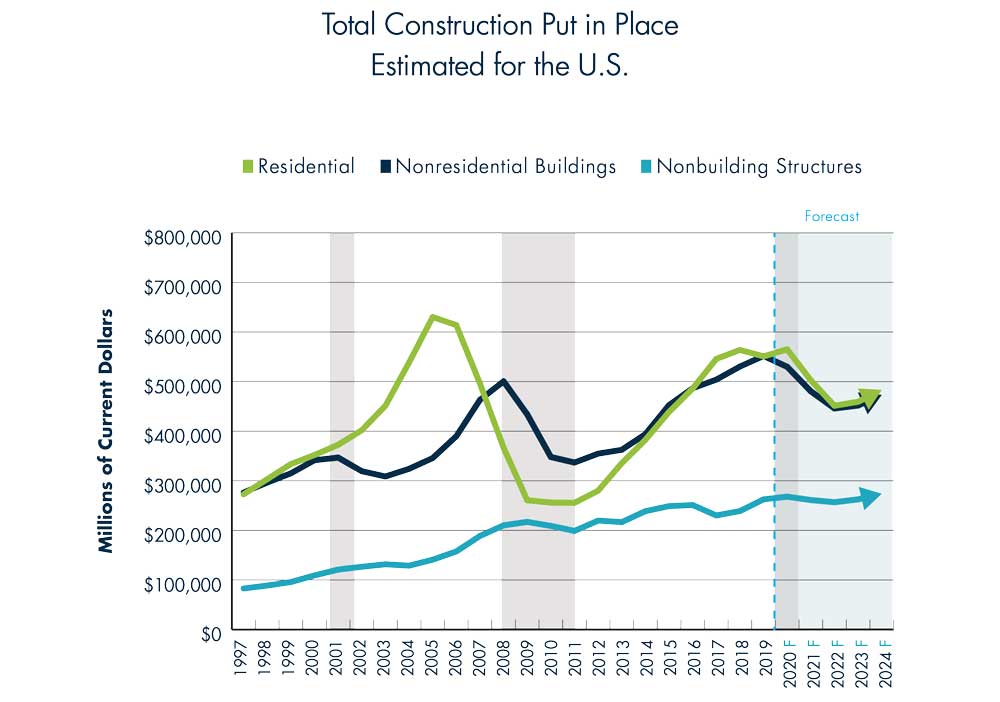

Even within sectors like construction, different parts of the country and different types of construction have witnessed different realities. For example, FMI research forecasts that total engineering and construction spending in the U.S. will end 2020 relatively flat, compared to 2 percent growth in 2019, but there is significant divergence between the residential and nonresidential building markets.

FMI Construction Outlook – What’s In Store for Water and Wastewater in 2020?

On the residential front, FMI predicts that single-family and multi-family building will end the year flat, driven by uncertain demand for large-scale, mixed-use developments and heightened unemployment. Despite this backdrop, builder confidence has proven resilient and remains at all-time highs. Improvements, on the other hand, will benefit from extended work-from-home mandates across many parts of the country, as well as a wave of refinancing spurred by continued accommodative interest rate policies.

FMI research suggests that residential construction put in place will contract sharply in 2021 and 2022 owing to continued unemployment pressure, the easing or cessation of government stimulus programs and bloated inventories.

The nonresidential space, while showing improvement from the second quarter of 2020, is still on a consistently downward trend. FMI’s third quarter Nonresidential Construction Index (NRCI) reading of 45.6 (scores above 50 indicate expansion) reflects fewer future engineering and construction opportunities.

Building segments such as religious, amusements and recreation, lodging, office and commercial are – predictably – suffering from major disruptions and declines in spend.

However, health care construction remains stable, and public safety is a rare nonresidential sector expected to have grown in 2020 on the back of rising crime rates and continued social unrest. Strained local and state budgets portend a modest contraction over the next couple of years.

RELATED: 2019 FMI Construction Outlook

Nonbuilding Structures – Wet Utilities

In broad terms, FMI believes that the nonbuilding segment of the construction industry will have held up relatively well in 2020. In the power sector, resiliency improvements, regulatory requirements and electrification trends are expected to help offset short and midterm losses in oil and gas spending.

Highway and street spending may benefit from a renewed focus on a holistic infrastructure package, but with Washington likely to remain divided and contentious after the recent election, it is unclear if faith in this prospect is realistic.

RELATED: FMI Construction Forecast – Direction for 2018

As oil prices are expected to remain low, and EPA budgets remain in contention, conservation and development construction is expected by FMI to drop off over the course of the next couple of years after ending 2020 up 2 percent.

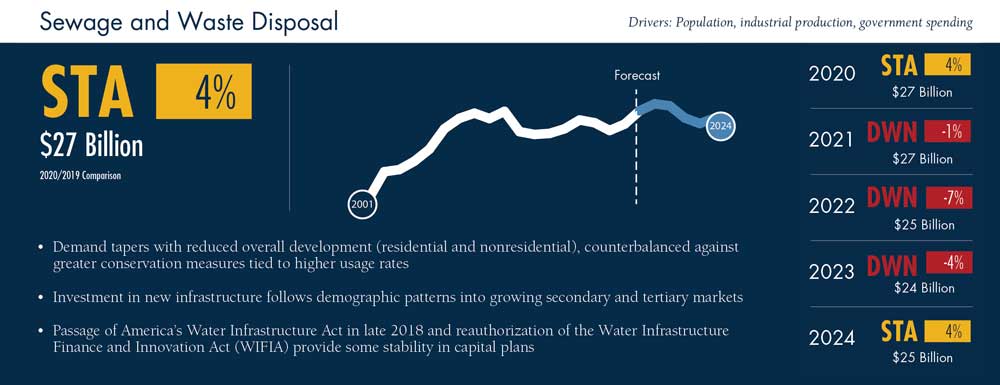

Narrowing in on the wet utility space (water and wastewater), a consistent narrative emerges, largely informed by population trends, industrial production, and government spending. FMI research forecasts that sewage and waste disposal is projected to grow 4 percent in 2020 before contracting in the years 2021-2023.

While the passage of America’s Water Infrastructure Act in 2018 still provides a measure of cover and stability for capital plans, depressed demand in both the residential and nonresidential spaces tempers the short-term outlook.

Though there is a demonstrated need for expansive investment and improvement in the U.S. water network, we believe that the spending trajectory over the next few years will not meet the need.

Water construction will end 2020 materially higher than 2019 — up 9 percent — but will be either stable or declining in each of the next threes years by FMI’s estimate. Even if borrowing costs remain attractive in the short-term, the strong current of demographic shifts into secondary and tertiary markets coupled with an eventual dissipation of government stimulus paint a challenging picture in the wet utility space in the short to medium term.

RELATED: FMI Construction Forecast – What’s In Store For 2017

2021 Outlook and Future Expectations

The information presented creates a challenging dynamic for the wet utility contractor. Despite the ASCE continuing to give near failing grades for the water infrastructure market, the urgency to repair infrastructure at the municipal level is lacking.

Creating new bond offerings to do large-scale repairs during a challenging economic cycle will be limited and municipal budgets are also depressed due to COVID-19 related expenditures and lower sales tax revenues. This puts the ball squarely in the hands of state and federal legislatures to create the regulatory framework that would require improvement and the financing to ensure it is possible.

While we are optimistic about the prospects for a meaningful infrastructure bill to come out of Congress in 2021, this will require coordination across the aisle that has not been present for the last four years. These factors are why FMI believes that the bid market will be very tight as contractors are looking to keep slightly profitable work to keep their employee base while waiting for the pressures of the pandemic to pass.

While this year will be challenging, the prospects remain quite interesting. We anticipate a rise in single-family construction as there is an increase in people working from home and staying away from metropolitan centers. We would also anticipate legislation to repair infrastructure and prevent the kind of tragedies that resulted in both criminal and civil lawsuits in places like Flint, Michigan. Lastly, there is ample work in other underground infrastructure segments (power, gas and communication) that will keep competition to those who specialize in wet utility construction.

Because of these drivers, cautious investment in growth and maintaining the workforce through 2021 will likely result in increased opportunities and growth in the future.